By Ruairi O'Shea

Former Investigative Writer | Kaituhi Mātoro

Scams are a big problem in New Zealand. But with the data on scams so poor – experts can’t agree whether we lose $200 million or $2 billion to scammers each year – it’s hard to know exactly how big.

So, we surveyed 1,200 New Zealanders about their experiences of scams, and what they think about the banks’ and government’s responses to the issue.

Here’s what we learnt.

1 in 5 people in New Zealand have been scammed

More than one in five of us have fallen victim to a scam related to our bank accounts or financial services, according to our survey.

We asked whether people have ever fallen victim to a scam, so we don’t know when these incidents took place. Some may be historic.

However, the NZ Crime and Victims Survey indicates the currency of the issue. According to this survey, in 2024, 14% of people experienced fraud and cybercrime.

That’s almost three times higher than the rate at which people reported experiencing theft and damage (5% in 2024).

We think that if 14% of us were experiencing physical theft each year, it would likely be one of the government’s top priorities. The government says it wants to be tough on crime, yet scams continue to go under its radar.

Older people are more likely to be scam victims

Scams are prevalent in every age group across New Zealand.

In our survey, at least 16% of every age group reported experiencing a scam related to their bank account or financial services.

Yet, while everyone needs to be vigilant, older consumers are more likely to fall victims to scams. Between the ages of 18 and 59, around 19% of New Zealanders have fallen victim to a scam. For those aged 60 and over, this figure jumps to 30%.

The cliche explanation is that older people are less savvy when it comes to technology, so less likely to spot the hallmarks of a scam. While there may be an element of truth in that stereotype, there’s another reason that older people are targeted by scammers.

They tend to have more money.

People feel positive about confirmation of payee

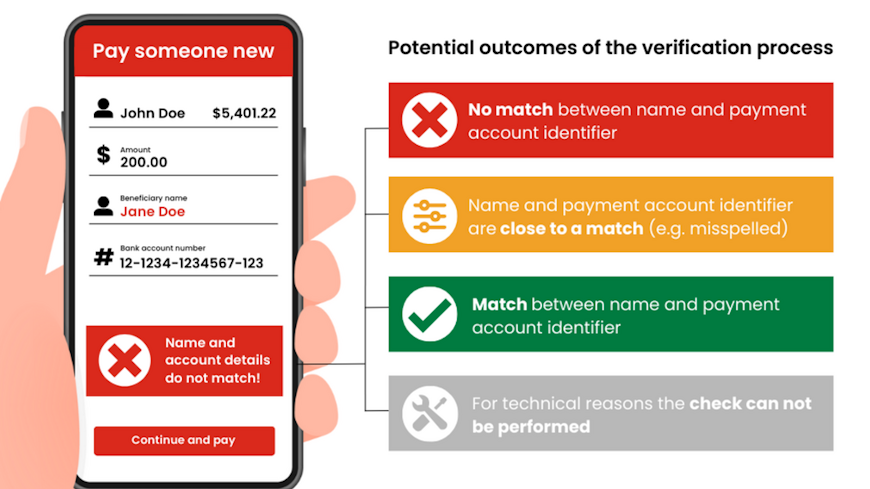

Seven years after it was first implemented in the Netherlands, banks in New Zealand began to rollout confirmation of payee in 2024. All banks should have this service implemented by Easter 2025.

Confirmation of payee identifies whether the name of a payee corresponds to the account number held by the bank. So, if a scammer tells a potential victim their name is John Doe, but the account belongs to Mr A Naughtyman, the bank can flag the discrepancy before a payment is completed and prevent a scam.

There’s no doubt confirmation of payee can add friction to making payments online. If you know someone by a nickname – Nick rather than Nicholas, for example – the service might flag it as a partial match and ask you to consider whether the payment is safe.

While this can be frustrating, or even scary, we think it’s a small price to pay for increased payment security.

The majority of consumers agree. In our survey, 69% of respondents said they’d had a positive experience using confirmation of payee. Almost half of respondents said their experience using the service was “very positive”.

Confirmation of payee is an important tool in our fight against scams, but it’s not a silver bullet, and vulnerabilities remain.

Victims can be persuaded into ignoring the warnings the service offers. Further, if an account is being used as a ‘mule account’, criminals can simply provide the correct name and account number to receive the payment, and then quickly transfer the proceeds overseas.

Reports have already reached us of consumers who have fallen prey to scammers even with confirmation of payee. We think there’s much more that banks can do to protect us.

Many think banks are doing a good job – they’re not

Consumers give banks much more credit than they deserve when it comes to scam prevention.

Almost two-thirds of consumers (62%) believe the scam prevention tools banks use in New Zealand are effective at preventing scams.

It’s true the banks have made some improvements in their security processes in recent years – removing links from text messages, targeting mule accounts, implementing confirmation of payee.

However, these measures have taken far too long to put in place.

It’s great that the banks have implemented confirmation of payee, but important to remember it came 7 years after it was introduced in Europe, and only after significant pressure.

New Zealand has also been left behind the rest of the world when it comes to payment technologies. It is the only country in the OECD not to have implemented, or committed to implementing, a real-time payments network. Most nations in Asia, South America and Africa have these networks in place, but Payments NZ – New Zealand’s bank-owned payments governance organisation – has failed to implement one here.

This means our payments are less secure and makes fraud harder to track through a payments network. It also makes consumers reliant on account-to-account services, like POLi, to make surcharge-free payments, even though these services breach many banks’ terms and conditions.

Consumers in New Zealand are forced to opt between saving money on surcharges and their banking security. This is a choice made by the banks, and consumers should not accept it.

84% believe the government should establish an anti-scam centre

Consumers are clear on who should take responsibility for establishing an anti-scam centre. The government.

Over 80% of our survey respondents agreed that the government should shoulder this responsibility. Unfortunately, the government is showing little appetite to lead the fight against scams.

In 2024, the then commerce and consumer affairs and anti-scam minister, Andew Bayly, wrote open letters to the banking, telecommunications and digital platforms industries urging them to tackle the scams crisis.

In response to Bayly’s letter, the banks correctly pointed out that the international practice is for governments to establish and own a centralised anti-scam centre.

We don’t agree with the banks on much, but Consumer NZ, our survey respondents and the banking industry is in agreement here. The government needs to take the lead to stamp out scams.

Stamp out scams

Scams are on the rise, with over a million households in NZ targeted by scammers in the past year. Help us put pressure on the government to introduce a national scam framework that holds businesses to account.

Our survey methodology

Our survey on scams was part of our Banking Satisfaction Survey. The online survey took place between 12 and 28 February 2025. It was based on a nationally representative sample of New Zealanders, aged 18 years and over, who have a personal bank account and KiwiSaver.