Consumer NZ surveying has found premiums for comprehensive car insurance have increased up to 38% since 2021.

Consumer is urging New Zealanders to shop around for their car insurance. Switching providers can save people hundreds of dollars per year.

This significant increase in premiums is likely due to the payout insurers faced after Cyclone Gabrielle as well as rising inflation.

“The more an insurer needs to pay out on claims, the more likely they’ll need to charge customers more,” explains Rebecca Styles, investigative team leader at Consumer.

Despite the price increase in premiums, Consumer's 2023 car insurance premium survey found that switching car insurance providers could result in a family of four saving up to $670 a year on average.

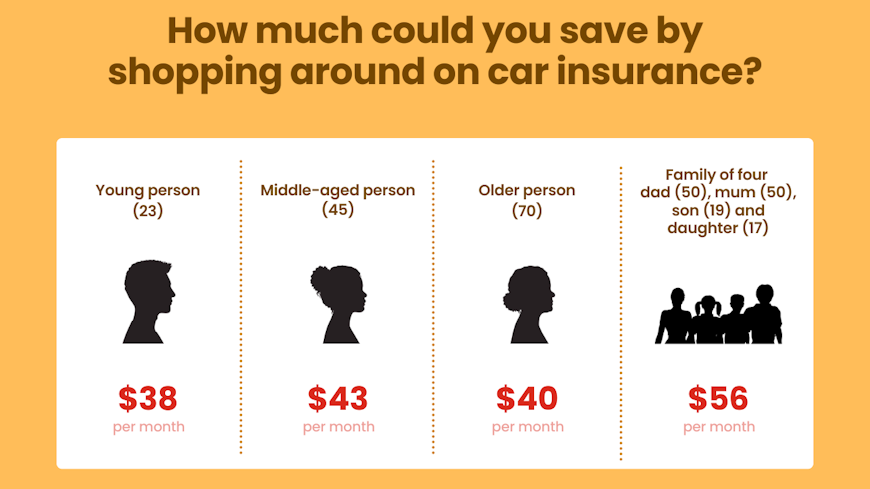

Consumer obtained car insurance quotes for four scenarios: a young, middle-aged, and older person and a family of four. While the lowest median insurance increase for an older person was 8%, it was up as much as 38% for a family of four.

“While there is a perception that all car insurance is the same, there are some differences between policies which could save you money.

“We found that younger people could save nearly $38 a month by shopping around, and older people could keep an extra $40 in their pocket.”

The cost of protection

Consumer’s 2023 insurance survey also found that among those without coverage, 10% chose to let their car insurance policy lapse due to cost – up from 2% in 2022.

“Insurance provides a crucial safety net, but the ongoing cost of living squeeze is pricing people out of insuring their car altogether.”

While some factors like the increased risk of extreme weather events or how long you’ve been driving are out of your control, Styles says there are still other levers you can use to pull your premium down.

"Insurance companies are constantly assessing the risk they’re taking on. Similarly, customers should also be assessing whether the insurance they’re paying for is right for their needs.”

How to make sure you’re getting the best value

1. Check your cover is right for you

Review the different types of coverage your insurance company offers to make sure your current level of coverage is right for your needs.

“It might be tempting to base your insurance decisions on price alone, but it’s important to understand the risks involved with each type of cover.

"Plus, people's circumstances change all the time. If you’ve started parking your car in a garage instead of the street or vice versa – change your cover to match your increased or decreased risk.”

2. Review the excess you pay

Increasing your excess can reduce your premiums. Just make sure that if the worst happens, you can afford to pay that excess.

3. Avoid add-on insurance products

These are often sold with car finance and don’t provide good value for customers.

“You already have protections under the Consumer Guarantees Act – we don’t recommend buying add-on insurances.”

4. Choose one insurer for a multi-policy discount

If you’ve got house, contents and car insurance spread out across different providers, you might be able to combine them with one insurer and get a multi-policy discount.

5. Pay annually for a discount

Can your budget stretch to paying your premium annually? A lump sum annual payment should get you a discount.